The Position of Taxation: An Islamic Perspective

Paper presented at the 7th Annual Lecture of Shooting Star of Islam – 1942

on Sunday, 20th April, 2025

at Ansar-Ud-Deen Grammar School, Surulere, Lagos State, Nigeria

By Star (Prince) Abdul-Rasaq ‘Kunle bin Abdul-QUADRI

Audhubillahi minashaetooni rojeem. Bisimillahi Rahmani Raheem. Ashiaadu anlaa ilaaa ilaha ilallahu. Wa ashiadu ana Muhammadu abduhu wa rosuuluhu.

I seek refuge with Allah from satan, the accursed one. In the name of Allah, the Beneficent, the Merciful. I bear witness that none is worthy of worship except Allah, Subuanohu Wa Taa’la. I also bear witness that Prophet Muhammad (Peace and Blessings of Allah be upon him) is the servant and apostle of Allah.

Protocols.

Let me salute the courage and sagacity of the founding members of Shooting Star of Islam (SSI) – 1942, who precisely 83 years ago, established this Islamic body with the aim of providing educational guidance for the indigent Muslim students. I pray that Allah (SWA) shall continue to grant them and other departed Muslims Aljanat-firdaous. Amin.

I also want to express gratitude to our late Star (Pa) Idris Lediju who moved and counseled at a general meeting of SSI that members of the association should be prepared to present lectures at the annual public lecture after the first lecture had been taken by Sheik Abdul-Hakeem Kosoko, an erudite scholar. This motion was unanimously adopted by the house and here we are today with the 7th edition of the annual lecture.

Permit me to quickly go back in history as the last time that I had the opportunity to address an audience in this hall from this position was 1977 in my capacity as the Assembly Prefect having then taken over from my brother Star (Dr.) Mustapha Sanbe who incidentally presented the 6th Annual Lecture on the 7th of July, 2024.

Alhamdulillahi, I can be said to be an expert in the subject of taxation (only by qualifications), but can this be said of the Islamic perspective of taxation? It is therefore pertinent to mention from the onset that I am least qualified to make this presentation as I am not an alim by any standard. To this extend, please accept this demonstration and appearance as being from someone who is ready to learn.

Taxation is a topic that is very dynamic and very often people are not willing to discuss possibly until issues are brought up. If I ask a question right now – who wants to pay tax WILLINGLY, for one reason or another, I may not get up to 5% in affirmative. This is not only in Nigeria but majorly in the developing communities. Once you are expected to payout, the debate gets hotter within the individual.

Two things are said to be certain in some climes – tax and death. The control within the tax system is so strong in those communities that you evade tax and go to jail, simple. Even in liquidation matters, tax obligation to government ranks highest. I have not said that people do not evade tax in those climes but the point remains that you must not be caught. Can one say that of a country like …? I still remember quite well in 2008 when I accompanied my then CITN President to South Africa Institute of Taxation’s (SAIT) conference in Johannesburg and the SAIT decided to host international delegates to a dinner. While delegates from other countries responded with over 80% tax compliance level, my then President was busy speaking big big grammar – reforms, policy development, at al. The rest, as they say is now history.

While I acknowledge the presence of taxation experts both within the hall and online, I will as much as possible avoid technicalities so that students of taxation particularly the students here can follow with ease.

In order to fully appreciate this discourse, I have decided to divide this paper into six parts as follows:

•Introduction and evolution of tax system.

•An insight into the fundamentals of tax system. •Taxpayers, government and social contract.

•Islamic perspective of taxation.

•Benefits of paying taxes.

•Conclusion.

1. Introduction and Evolution of Tax System

In as much as there are human beings on earth, tax remains the only sustainable source for the government to generate income for the purpose of delivery of dividend of governance. Other income from oil, mineral resources, etc. are bound to expire or become obsolete. It is therefore important that sufficient attention be given to this revenue type which is a creature of statute and by representation too.

– Taxation in the Medieval Age

In the early period, the king and chiefs who have the political and administrative powers within the community promulgated the tax laws basically for governance and upkeep of the king and chiefs. Taxes paid are measured in line with the wealth of individuals such as land, poultry, livestock and animals and farm products, slaves, etc. This style of taxation is known as

feudal system, very outdated. In the northern part of Nigeria, tax was levied on movable properties to provide alms for the poor, needy, widows, etc.

Another significant form of taxation in the medieval period is the tithe amounting to one-tenth of a person’s produce or income. This was predominant under the influence of the Church and seen as a religious tax up till today.

Other types of taxes in the old age include scutage paid in lieu of military service and to prosecute wars and tallage on tenants in respect of landed properties.

From the above, the subject, taxation is not new but had since grown in bounds from the old age and tax laws are now more by representation while administration gone digital.

By virtue of Section 24(f), of the Nigerian Constitution (as altered), every citizen is expected to declare his income honestly to appropriate and lawful agencies and pay his tax promptly. Only the National Assembly can pass tax bills in Nigeria and become law on the ascent of the President. This is different from tax administration. While the NASS provides the body of rules or commandments that must be followed, the tax administrators ensure the correct implementation of the tax laws.

– Definition and Need for Taxation

Simply put, a tax is a compulsory payment levied on the citizens by the government for the purpose of achieving its goals.

– Taxes and other payments

There is need to distinguish between tax from other payments made by the citizens to the various levels of governments such as permits, charges, fees, fines, etc. A simple definition of tax had been made, some other payments to the governments may look like tax but in most cases directed to provision of a particular service e.g. Land Use Charge, fee for procurement of international passports/driver’s licence, etc. Another distinguishing difference is that taxes are collected for the development of the community in communal areas such as security, health, education, infrastructure, etc. while the payer gets the direct benefits for fees, charges, etc. On the other hand, fines and penalties are sanctions for breaking the laws.

– Forms of Taxes

Taxes can be classified into various forms. Examples are briefly discussed below.

Proportional Tax. This occurs when the proportion paid by each taxpayer bears the same ratio to the amount to be raised as the value of his property bears to the total taxable income.

Progressive Tax. This graduates to apply higher rates of tax as income increases. The principle here is that there is bound to be redistribution of income from the well-to-do to the less privileged. The only demerit of this type of tax is that it may discourage the spirit of enterprise or hard work.

Regressive Tax. The structure is such that the tax yield becomes smaller as the value of the property taxed increases. This is not suitable for a developing country as it fails to provide a just and egalitarian society.

Presumptive Tax. This is a tax that is set out to encourage a taxpayer to imbibe tax-paying culture. Often used within the informal sector where for all practical purposes, the income of a person chargeable to tax cannot be ascertained or records are not kept in such a manner as to enable proper assessment of income. This may be negotiated or final Direct Tax. This is demanded and paid by the person who it is intended or desired to pay it. The burden of payment falls squarely on the taxpayer and cannot be shifted to someone else. This would ordinarily include taxes on income and capital.

Indirect Taxes. This is demanded from one person with the intention that he/she shall be indemnified by another. Majorly, these are taxes imposed on commodities and are paid by the consumers not as taxes but as part of the price of the item. Examples are Excise Duty, Value Added Tax, Sales Tax, Stamp Duty, Customs Duty, etc.

– The need for taxes

The need for taxes would best be described as follows:

i. To raise money in order to meet government expenditure;

ii. To redistribute income and wealth in order to reduce inequality; and

iii. To plan and direct the economy by shaping the economic growth and development of the country. To this extent, taxation is important in the planning of savings and investment.

2. An Insight into the Fundamentals of Tax System

A good tax system stands firmly on a tripod i.e. tax policy, law and administration. Of recent, the taxpayers have been added as a fourth leg since they are regarded as the KINGS!

Tax policies are fundamental guidelines for the establishment of the tax laws and administration. The laws are promulgated by the relevant legislative authorities and the administrators implement the letters of the laws.

Basically, a good tax system should have five (5) attributes. These are:

Universality. The liability for tax should cover all citizens and all embracing. The principle of equity means that those with the same income pay equal amount of tax while those with different income pay different amount of tax.

Certainty. There should be certainty with regards to amount and timing of tax due.

Convenience. The time and manner of payment must be convenient to the tax payer.

Economy. The system of collection must be economical. There should be administrative efficiency while relating the revenue raised with the cost of collection.

Infrastructural development. There must be judicious expenditure of taxes collected so that misuse of funds would not constitute disincentive for compliance.

– The dynamic nature of taxation

There is always the need regularly to review the tax system of any community to ensure that it conforms with the best practice. This review should however be such that had been planned and not haphazard. This paper would not be complete without a peep into the reforms in the Nigerian tax system and particularly the recent tax reform introduced by the Federal Government which should have come up many years back as quite a lot of the provisions in the law are archaic and do not meet the standard required.

In 2023, the Federal Government of Nigeria set up Fiscal Policy and Tax Reforms Committee headed by Mr. Taiwo Oyedele. The result of the many months of meetings and engagements of stakeholders is the four bills that were submitted to the two arms of the National Assembly in 2024.

While commending the efforts of all stakeholders, two compelling issues are the dark sides that should be urgently looked into. The first is the issue of professionalism which has been watered down and the envisaged movement from direct taxation to indirect taxation that seem to have been dumped. The earlier we get this right, the better for all.

I will pause here with this quote from the Holy Book:

– Allah (SWA) commands in the Holy Qur’an, 4:59

O ye who believe! Obey Allah and obey the Apostle and those in authority from among you…

As already established, governments must fund their activities in one way or the other within the laws of the land. The definition of tax earlier given in this presentation is to a large extent to obey the authorities. Therefore, delivery of civic responsibilities including settlement of taxes constitutes an obedience to Allah’s commandment.

3. Taxpayers, Government and Social Contract

A social contract exists between the government and the taxpayer following the mutual obligations and responsibilities that exist between the two. While the taxpayer is expected to honestly declare and file returns to the best of his knowledge and settle the tax due, it is anticipated that the government shall utilise the revenue collected responsibly, efficiently and judiciously to fund public goods and services such as infrastructure, defence, healthcare and generally promote the well-being of its citizens. It behooves on the administration to seamlessly account for all revenues collected. The obligations between the taxpayer and the government which form the cornerstone of connection is called Social Contract. This relationship is based on the understanding that citizens will contribute portions of their income through taxes, and in exchange, the state will use these funds to benefit society as a whole.

– Which comes first, the egg or chicken?

Would the citizen wait on the government to provide facilities before payment of taxes? I strongly believe that the taxpayers should play their part while government makes judicious use of monies collected. Asking questions regarding revenue collected by government is not anti-government but holding government responsible and accountable.

– Responsible Governance and Voluntary Compliance

One of the cardinal principles of taxation is to create an environment for voluntary compliance by the taxpayer. What has been discovered is that it is when the leadership of the State delivers the dividends of democracy and the citizens can physically see them, then, compliance would be more assured. An average taxpayer has become skeptical of the intentions of political leadership (tax spenders) that the only way they could be encouraged to comply is where governance is brought to their doorstep.

Compliance with tax laws comes along with its sanctions in respect of default which may be intentional or unintentional. It behooves on the taxpayer to jettison acts conflicting to prevailing laws and regulations and abide with fundamental principles of integrity and professional behavious. The way out for the revenue is to establish robust monitoring processes, training and retraining of personnel and evolve policies that would aid compliance. The cost of noncompliance may include legal issues, financial sanctions and damage to reputation.

4. Islamic Perspective of Taxation

– Zakat, a Pillar of Islam

Zakat, also referred to as poor-rate is an Arabic word that means growth or distillation or purification. The fourth pillar of Islam is payment of Zakat as sanctioned by Allah (SWA) in the Holy Qur’an 9:60.

Alms are only for the poor and the needy, and the officials (appointed) over them and those whose heart are made to incline (to truth) and the (ransoming of) captives and those in debts and in the way of Allah and the wayfarer; an ordinance from Allah; and Allah is knowing and wise

In essence, Zakat (payment of poor-rate) is an obligation from Allah, an injunction that must be complied with. The verse of the Holy Qur’an quoted above established those who should benefit from Zakat, the Book went forward to emphasise the importance of Zakat in many verses including:

Holy Qur’an 2:43 – And keep up prayer and pay the poor rate… Holy Qur’an 2:83 – … and keep up prayer and pay the poor-rate… Holy Qur’an 2:110 – And keep up prayer and pay the poor-rate… Holy Qur’an 2:177- … and keep up prayer and pay the poor-rate…

Holy Qur’an 2:277 – …and do good deeds and keep up prayer and pay the poor rate…

Holy Qur’an 4:162 – …and those who give up prayers and those who give the poor-rate…

Holy Qur’an 4:55 – …those who keep up prayers and pay the poor-rate…

Holy Qur’an 7:156 – …so I will ordain it (specially) for those who guard (against

evil) and pay poor-rate…

Holy Qur’an 9:5 – …and keep up prayer and pay poor-rate…

Holy Qur’an 9:11 – …and keep up prayer and pay poor-rate…

Holy Qur’an 9:18 – …and keeps up prayer and pays the poor-rate…

Holy Qur’an 9:71 – …and keep up prayer and pay poor-rate…

Holy Qur’an 19:31 – …He has enjoined on me prayer and poor-rate… Holy Qur’an 21:73 – …and keeping up prayer and pay poor-rate…

Holy Qur’an 22:41 – …will keep up prayer and pay poor-rate…

Holy Qur’an 22:78 – …therefore keep up prayer and pay the poor-rate… Holy Qur’an 24:37 – …and keeping up of prayer and giving of poor rate… Holy Qur’an 24:56 – And keep up prayer and pay the poor-rate…

Holy Qur’an 27:3 – Who keep up prayer and pay the poor-rate…

Holy Qur’an 30:39 – And whatever you lay out as interest so that it may increase in the property of men, it shall not increase with Allah; and whatever you give in Zakat desiring Allah’s pleasure – it is these (persons) that shall get in manifold.

Holy Qur’an 31:4 – Those who keep up prayer and pay the poor-rate… Holy Qur’an 33:33 – …and keep up prayer and pay poor-rate…

Holy Qur’an 58:13 – …and keep up prayer and pay poor-rate…

Holy Qur’an 98:5 – …and keep up prayer and pay the poor-rate…

The demonstration of Salat along with Zakat in the verses of the Holy Qur’an above is not mere coincidence but a manifestation of the importance of charity to showcase the inner-will in the followership and demonstration of our faith. This, to a large extent helps in the development of the system, structure and people as prescribed by Allah (SWA).

There is no doubt that Zakat as emphasised in many verses of the Holy Qur’an as obligatory and indeed the fourth pillar of Islam, a deviation from which there are sanctions. May Allah (SWA) guide us aright. Amin.

The Hadith of the Holy Prophet (PBUH) equally admonishes Muslims on the payment of Zakat. Some of the Hadiths are summarised below:

Sahih Bukhari: One who pays Zakat, Allah will make their wealth increase Sahih Bukhari: Zakat purifies one’s wealth Sahih Bukhari: Zakat is a right that the poor have upon the rich Sahih Bukhari, Vol 2, Book 24, No. 491 – If one gives in charity what equals (the size of) one date-fruit from the honestly-earned money and Allah accepts only the honestly earned money –Allah takes it in His right (hand) and then enlarges its reward for that person (who has given it), as anyone of you brings up his baby horse, so much so that it becomes as big as a mountain.

Sahih Bukhari Book 5, 2178: Allah says, ‘Spend, O son of Adam, and I shall spend on you. The right hand of Allah is full and overflowing and in nothing would diminish it, by overspending day and night.

Sahih Bukhari, Vol 2, Book 24, No. 490: There is no envy except in two: a person whom Allah has given wealth and he spends it in the right way, and a person whom Allah has given wisdom (i.e. religious knowledge) and he gives his decisions accordingly and teaches it to the others.

Al-Trimidhi, Chapter 7, No. 618: When you pay the Zakat you have fulfilled what is required of you.

Al-Trimidhi, Hadith No. 2247: The best charity is to satisfy a hungry person. He also said, “No wealth (of a servant of Allah) is decreased because of charity.”

Sahih Bukhari: Giving charity wipes away sins just as water extinguishes fire.

Sahih Bukhari: Giving Zakat is more beloved to Allah than giving in charity during the entire year

Sahih Bukhari: Zakat is a form of worship, and the one who fulfills it will be rewarded

Sahih Bukhari: The one who pays Zakat, it is as if they have freed a slave

The importance of paying Zakat cannot be overemphasised and the prayer is

that Allah (SWA) keeps us among the righteous. Amin.

– Consequences of Unpaid Zakat

It has been established that payment of Zakat is an obligation as ordered by Allah (SWA). The Holy Qur’an 3:180 says:

And let not those deem, who are niggardly in giving away that which Allah has granted them out of His grace, that it is good for them; nay, it is worse for them, they shall have that whereof they were niggardly made to cleave to their necks on the resurrection day; and Allah’s is the heritage of the heavens and earth; and Allah is aware of what you do. (Allahu Akbar)

The import of the above is that the unpaid Zakat is a debt owed and better settled while alive and Allah (SWA), the Judge is ultimately the Witness! May Allah (SWA) guide us aright. Amin.

There is no additional fine or interest or penalty for one who missed Zakat other than to hurry to pay the outstanding Zakat and seek repentance from Allah (SWA).

– How to Compute Zakat

Zakat surpasses individual or entity’s charitable organisation as it is a spiritual financial compulsion. Zakat which is aimed at purifying one’s wealth and supporting societal development. As would be seen later, it should be noted that payment of Zakat would not debar one from other state taxes.

Zakat is calculated as 2.5% of Zakat base. The Zakat base is defined as the net worth of the individual on the date of payment. It follows therefore that Zakat rate shall only be levied on the wealth of the individual. The net worth of the individual is computed as all assets excluding fixed assets used in operations but including savings, jewelries, silver and investment less short term payable and excluding future expenses which do not fall within the next 12 lunar months. For an individual to be eligible – Nisab, the personal wealth must be above the Nisab threshold of 85g of gold or 595g of silver or equivalent. Where the wealth is negative or below the Nisab threshold during a particular year, the new Zakat year is reset. Zakat is not paid unless the person passes the Nisab threshold when a new year begins.

Other forms of Zakat such as farm produce and livestock

•Farm produce

Zakat on farm produce or agricultural Zakat is calculated based on the method of irrigation vis a vis the amount of produce as follows:

– 10% rate for rain-fed crops; and

– 5% for those irrigated with efforts

This payment shall be due at the time of every harvest.

•Livestock

Zakat on livestock is due on camels, cattle and sheep including goats. The obligation arises when the number of livestock reaches a specific minimum threshold known as Nisab i.e.

For Sheep:

– Between 40 and 120, one-year old animal

– Between 121 and 200, two – 1-year old animals

– Between 201 and 399, three – 1-year old animals

– 400, Four – 1-year-old animals

– On every 100 thereafter, add 1

For Camel:

– For every 5 camels and up to 20, one 2-year old goat or 1 1-year old sheep.

– For every 25 camels, one 1-year old female camel is due.

For Cattle:

– For every 30 cows, one 1-year old calf is due.

– For every 40 cows, one 2-year old calf due.

While Zakat would not be due on horses, mules or donkeys except they are used for commercial purposes, some scholars are of the opinion that monetary value of the animal (as due) could be paid in the stead of giving animals themselves. This is done every full Hijri year.

– Who should receive Zakat?

Categories of people that should collect Zakat has been stated earlier with reference to the Holy Qur’an 9:60 in this paper.

– When is Zakat paid?

It is not true that Zakat should only be paid during the month of Ramadan. The Zakat is due once in a lunar year once a Muslim is within the Nisab threshold. There is need to establish when the Muslim first reaches Nisab threshold and subsequently every lunar year. This ensures regularity and timeliness should be the watch word. There is need to:

•keep adequate financial records;

•set a reminder few weeks before the due date; and

•plan, well in advance, to pay on due date to avoid procrastination.

Where not sure, there will be need to consult an Islamic Scholar or financial adviser who is knowledgeable in Islamic finance.

– Administration of Zakat

It is the practice of the Prophet (PBUH) to appoint his trusted companion to collect and distribute Zakat. Some Muslim countries now have administrative organs such as Zakat, Tax and Customs Authority in Saudi Arabia.

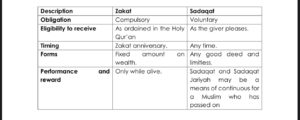

– Distinguishing Between Zakat, Sadaqah

Zakat should not be mixed up with Sadaqah and the major differences are tabulated below:

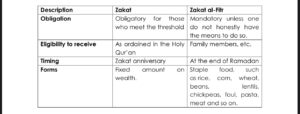

– Differences between Zakat and Zakat al-Fitr

We shall also tabulate the distinguishing factors between Zakat and Zakat al- Fitria.

- Other forms of ancient taxes

The Wikipedia describes the following as other forms of taxes established in the early days –

Jizya – a per capita yearly tax historically levied by Islamic states on certain non-Muslim subjects—dhimmis—permanently residing in Muslim lands under Islamic law, the tax excluded the poor, women, children and the elderly.

Kharaj – a land tax initially imposed only on non-Muslims but soon after mandated for Muslims as well.

Ushr – a 10% tax on the harvests of irrigated land and 10% tax on harvest from rain-watered land and 5% on Land dependent on well water. The term has also been used for a 10% tax on merchandise imported from states that taxed the Muslims on their products. Caliph `Umar ibn Al-Khattāb was the first Muslim ruler to levy ushr.

Khums (Arabic: ُخ ْمس Arabic pronunciation: [xums]) a tax of one-fifth (20%) of wealth acquired as the spoils of war; and, according to most Muslim jurists, other specified types of income, towards various designated beneficiaries. In Islamic legal terminology, “spoils of war” (al-ghanima) refers to property and wealth looted by the Muslim army after battling with or raiding non-Muslims.

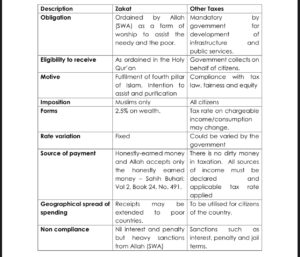

– Differences between Zakat and Other Taxes

Several types of taxes have various features and impositions depending on their nature. There are distinguishing differences between Zakat and other taxes as in the table below:

Need to generate more funds through taxation

Funds must be raised for governance and some Muslim countries, seeing the inadequacies of taxes collected, introduced other taxes such as:

•Personal income tax

•Company income tax

•Consumption taxes including Value Added Tax, Excise Duty, Custom Duty, etc.

5. Benefits of Paying Taxes

Generally, the act of giving is not only a financial obligation but also carries psychological and spiritual dimensions. Below are some benefits of paying taxes:

•Spiritual fulfillment: Payment of taxes is seen as act of worship and a means of purifying one’s wealth. For Muslims, fulfilling their Zakat obligation is a way to strengthen their connection with Allah, seeking spiritual fulfillment and adhering to one of the Five Pillars of Islam.

•Gratitude and humility: Taxes paid encourages gratitude for the blessings one has received. By giving to those less fortunate, individuals express gratitude for their own prosperity and acknowledge that their wealth is a gift from Allah. This instils humility and prevents arrogance or pride associated with material success.

•Equality and social justice: The psychological impact of taxes is evident in its role in promoting social justice and economic equality. Knowing that their contributions directly benefit those in need, individuals experience a sense of empowerment in addressing societal imbalances. This fosters a collective commitment to reducing poverty and inequality.

•Community bonding: The communal aspect of tax contributes to a sense of belonging within the Muslim community. By collectively participating in the practice of paying taxes, individuals and entities strengthen their ties with fellow community members, fostering a sense of unity and mutual support.

•Sense of social responsibility: As seen earlier, payment of taxes is deeply rooted in the concept of social responsibility. The psychological impact lies in recognising and fulfilling one’s duty to contribute to the welfare of society. This fosters a sense of accountability for the well-being of others and strengthens the communal bonds within the community. It emphasises the right to ask questions and demand for answers.

•Wealth purification: The act of giving is a symbolic gesture of purifying one’s wealth. It reflects an acknowledgment that all wealth ultimately belongs to Allah, and individuals are merely stewards of their possessions. By parting with a portion of one’s wealth, a devotee purifies the heart

from attachment to material possessions and cultivate a sense of detachment from worldly desires.

•Alleviation of guilt: For those with wealth, Zakat serves as a means to alleviate any feelings of guilt associated with material abundance. The act of giving becomes a mechanism for addressing the moral and ethical implications of wealth disparity and sharing resources with those in need.

•Psychological well-being: Research suggests that acts of altruism and charitable giving are associated with improved psychological well- being. The sense of purpose, fulfillment, and happiness derived from helping others can positively impact an individual’s mental health.

6. Conclusion

This paper has established taxation as the source of income to governments for the purpose of running their activities and the need for government to be accountable to the citizens. This is social responsibility contract that exists between the citizens and government. The only way voluntary compliance can be achieved, by judicious use of revenue collected. This part shall be achieved only when the citizens had played their part by honestly declaring and paying the taxes due and ask questions.

The revenue has no choice but to simplify the tax laws removing as much as practicable ambiguity and create good working environment for the administrators to strive. Revenue agencies should increase interactions with taxpayers, collaborate with civil societies and organisations including tax advocacy groups.

There is need to inculcate the need to pay tax from the lower forms as the level of education with respect to taxation remains very low. I acknowledge the efforts of Chartered Institute of Taxation of Nigeria which has yielded fruitful results with taxation now being studied as a discipline at the undergraduate, post graduate and doctorate levels in the universities and national diploma and higher national diploma at the polytechnics. The establishment of a Tax Academy by the institute is a welcome idea.

It will be a matter of interest if taxation curricular are developed for students of primary and secondary schools. The earlier we catch them young, the better.

The paper also opined that as Muslims, we have no choice but to comply with the injunctions of Allah (SWA) including payment of Zakat and we continue to

call on Allah (SWA) for guidance always. It is not a request but an obligation with serious repercussions on default.

There is need to inculcate the need to pay tax from the lower forms as the level of education with respect to taxation remains very low. I acknowledge the efforts of Chartered Institute of Taxation of Nigeria which has yielded fruitful results with taxation now being studied as a discipline at the undergraduate, post graduate and doctorate levels in the universities and national diploma and higher national diploma at the polytechnics. The establishment of a Tax Academy by the institute is a welcome idea.

It will be a matter of interest if taxation curricular are developed for students of primary and secondary schools. The earlier we catch them young, the better.

The paper also opined that as Muslims, we have no choice but to comply with the injunctions of Allah (SWA) including payment of Zakat and we continue to call on Allah (SWA) for guidance always. It is not a request but an obligation with serious repercussions on default.

To the Shooting Star of Islam – 1942, I give kudos for organising this session. We need this type of lectures to educate ourselves and I appreciate Shooting Star of Islam -1942 for this worthy course.

I will leave you with this mandate from Allah (SWA) in the Holy Quran 51:19 And in their property was a portion due to him who begs and to him who is denied (good).

May Allah (SWA) continue to guide us aright. Amin.

SubuanaLlaha wa biamdih

Astagfur Llah wa tuibiLlah

Subahana Rabika…

I thank you most sincerely for your patience and listening.

RAQ 200425

•References:

The Holy Qur’an

Qur’an verses on Zakat – My Islam

The Constitution of the Federal Government of Nigeria (as altered)

Hadith Explaining the Importance of Zakat in Islam – Transparent Hands

Islamic Zakat Calculator – Learn More About Zakat – Hard Relief

Importance of Zakat in Islam – Sahlah Academy

Obligatory charity tax (Zakat) – Sunnah.com

Differences between Zakat and Tax – Fincyclopedia

Zakat vs Tax: Difference and Comparison – Emma Smith

The Nigerian Tax System & Reforms – Prince Rasaq ‘Kunle Quadri

Contemporary Issues in Nigerian Tax Administration System – Prince Rasaq ‘Kunle Quadri

Zakah Administration and its Importance: A Review – Adamu Ummukhayr, Musa Yusuf Owoyemi and Rafidah Mohammad Cusair

The Impact of Taxation and the Quest for Good Governance: Evidence from Nigeria – A. A. Kifordu, Florence Konye Igweh and Aloamaka Judith Ifeaanyi

Rights and duties in Islam – Muhammad ibn Sâleh Al Uthaymîn

Further review of the paper The Position of Taxation: An Islamic Perspective – Ustaz Hakeem Olapade